yitech

-

Posts

146 -

Joined

-

Last visited

yitech's Achievements

")

Newbie (1/14)

0

Reputation

-

Transcript: https://seekingalpha.com/article/4070977-liberty-globals-lilak-ceo-mike-fries-q1-2017-results-earnings-call-transcript

-

Liberty Interactive Enters into Agreement to Acquire General Communication, Inc., Combine with Liberty Ventures Group and Split-off Combined Company from Liberty Interactive http://www.businesswire.com/news/home/20170404005774/en/

-

Doesn't Priceline own 10%+ of Ctrip? How is this going to fly with the justice department?

-

Commerce Hub S1 https://www.sec.gov/Archives/edgar/data/1665658/000104746916011805/a2227352zs-1.htm

-

The discounts right now are as follows: 1. LSXMK - 16% (assuming net debt is 200) NAV - $12.1B, MC - $10.2B 2. Braves - 12% NAV - $1b (nets rights offering at today's price less 20% against the interco) and MC - $901M adjusted for $200M rights 3. Media - 11.4% - NAV - $1.6B MC - $1.7B I think discount for LSXMK is only 11.5% since you need to compare (12.1B-0.2B) vs 10.6B. Margin debt has the first claim over SIRI.

-

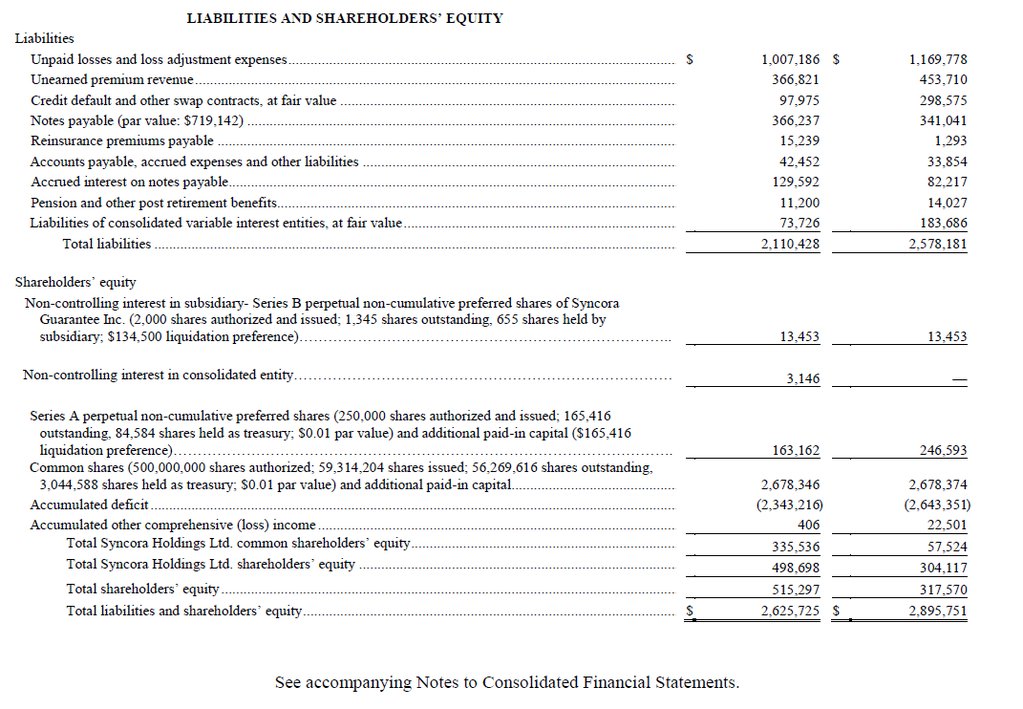

Syncora book value went up 6-fold YoY (from $1.02 to $5.96) with 56.3M shares outstanding.

-

Anyone still long this name? Baupost still owns ~ 14%. Merger spread with ChipMos Taiwan is about 40%. 3.71+34.9*18.71/32.83 ~ $23.6 vs $16.8 now. http://www.prnewswire.com/news-releases/chipmos-bermuda-and-chipmos-taiwan-agree-to-merge-chipmos-bermuda-holders-to-receive-us1977-in-cash-and-stock-for-each-chipmos-bermuda-common-share-300207710.html 8150.TW price is here: https://beta.finance.yahoo.com/quote/8150.TW The deal is scheduled to close in Q3.

-

It seems cash + investment roughly are slightly more than the long term debt (681M vs 640M). Assume they are the same and the end-game is LTPRA/B merging with TRIP, the capital gain tax liabilities disappear. I think Liberty Trip A shares are trading at 21% discount.

-

Just to add to that. SCHW deposit has been growing rapidly in the last few years. Bank deposit was up 26% YoY. More low-cost funding, but I guess it means nothing if interest rates don't rise. True earning power could stay low for a while.

-

How about this two statements from business plan update: "Low gas prices now seen as permanent condition" and "Market shift from cars to trucks and UVs now seen as permanent shift in demand" Are they making a macro judgement call on future oil prices?

-

Could this potentially cheapen the Jeep brand?

-

Was American the Wrong Airline for Spirit to Engage in a Fare War? http://www.thestreet.com/story/13387808/1/was-american-the-wrong-airline-for-spirit-to-engage-in-a-fare-war.html

-

I also got in around $36.3. The business model looks robust to me. Longer term this could be the next Ryanair / Southwest. I don't think pricing pressure from AAL would last indefinitely. They do have shareholders to answer to.

-

When you said tax-free status for spinning off a holding company that basically just holds stock, do you mean no cash tax and the underlying stock would compound pre-tax with deferred capital gain tax still accruing until it is sold or taken over (i.e. by some other company or Expedia)? I thought tax-free (cash tax and future tax liability) only applies to pure operating business spin-off. I am still a bit confused in this area. Hopefully someone can enlighten me..

-

They're only tracking stocks as opposed to a full split of the legal structure so DTL's should be unaffected. Right. I guess just tracking stocks so taking over of SIRI is most likely still the end game.