jschembs

-

Posts

437 -

Joined

-

Last visited

jschembs's Achievements

")

Newbie (1/14)

0

Reputation

-

I wonder how much overlap there is in SHOP's target customers with those that FB is targeting. I remember reading about FB's efforts to embed the click-to-buy functionality within IG, and thinking how that could really hurt SHOP. Obviously hasn't hurt SHOP's growth or stock price thus far.

-

I have made this a 5% position in the past 2 weeks. John Huber wrote about it in 2018 and the core thesis is very much in tact in my mind. https://sabercapitalmgt.com/facebook-is-undervalued/ Curious why you think they have a "very long runway ahead" (quote from Huber's post)? While there are some Google-esque "bets" with call-option characteristics, largely the success of the investment is based on user and ARPU growth in their core (legacy FB and Instagram) platforms, no? The core FB platform seems oversaturated with ads and (my opinion) unlikely to be the place to be for younger cohorts. Even IG seems to be saturating user feeds with ads. The business has done an admirable job staving off the MySpace extinction event, but what's the thesis for both of these platforms to deliver long-term growth?

-

Now Roku is at $60 billion rather than $22 billion. I've had a Roku for many years, and use it to search across my streaming subscriptions. It's UI is also simple enough to use. But why can't the big broadband companies take this business for themselves with devices like this: https://www.xfinity.com/learn/flex Totally agree. Seems that Roku's strategy now is to (a) increasingly flex their muscle as the middleman to extract higher fees from the content providers and (b) build their own content. Both seem very risky relative to their core competency. Anecdotally, we bought a Sony TV w/Android as the OS a year or so ago. Had a Roku stick plugged in, but couldn't get the cords to hide very well, so took it out and tried out the native smart platform in the TV. Frankly haven't noticed a difference in accessing what we would've on Roku, and it's far more seamless of an experience since it's built into the TV / remote.

-

Amazing post. The most comical aspect of all of this WSB shit to me is that it's ending up bailing out deep value guys who rode most of this stuff down to the point where it was effectively stub value. And I say that as a deep value guy who unfortunately didn't own any of these fun exit trades. QFT. If only Sears had managed to last to Jan 2021... ;D Ain't that the truth. SHLD and JCP would've been some amazing charts. Edit: nevermind, didn't realize SHLDQ still trades - of course, that was up 113% today.

-

Amazing post. The most comical aspect of all of this WSB shit to me is that it's ending up bailing out deep value guys who rode most of this stuff down to the point where it was effectively stub value. And I say that as a deep value guy who unfortunately didn't own any of these fun exit trades.

-

So true. Looking at names like Pitney Bowes and Express, two awful businesses, spiking on the WSB game, is just amazing. On the other hand, on a relative value basis, these things are really cheap trading at ~1x revenue vs SNOW and other SAAS plays. /s

-

100% cash purchase

-

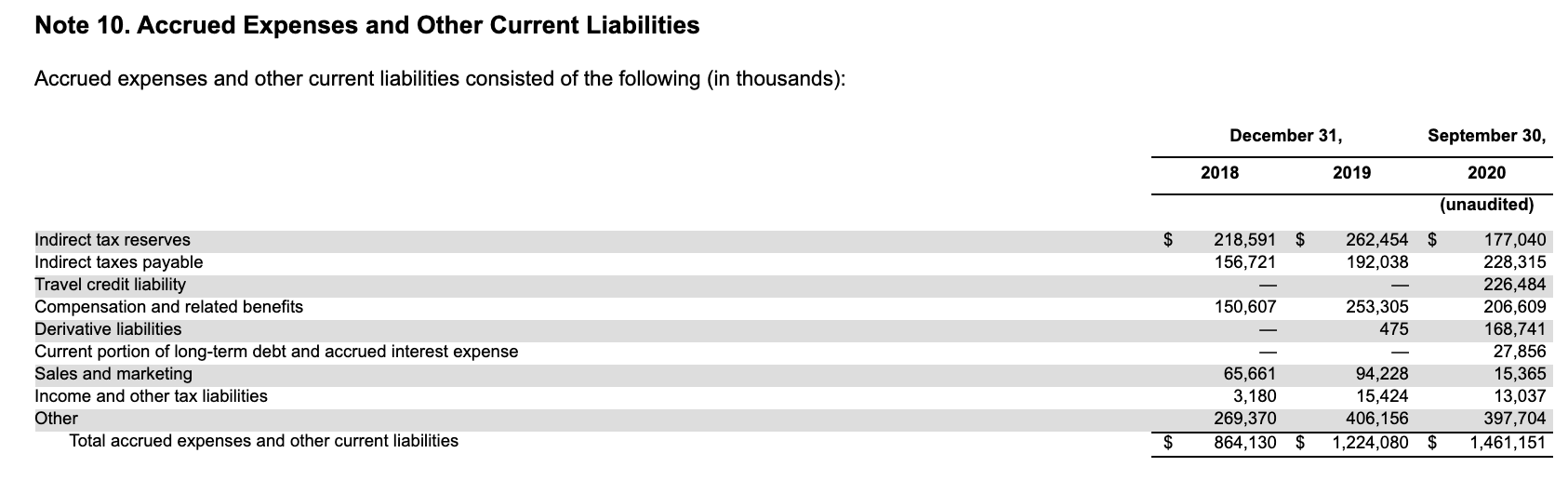

Any idea what the "other" category is comprised of within accrued expenses and other current liabilities? Bulk of their cash flow comes from collecting sales and other business taxes long before they need to be remitted, a wonderful float.

-

Doesn't 30k recall represent nearly 100% of the cars they sold in China in that time period? It would only be about 10% for GM's worst recall. Either way, the fix isn't particularly expensive. I'm very curious if this stays contained to China. I'm saying recalls are nothing out of the ordinary, and I'm surprised there weren't more for the early cars made in 2012-2013-2014... The company is basically a startup at that point, it's amazing that the Model S was as good as it was right out of the gate in 2012. Would generally agree with this, but obviously important to differentiate Subaru recalling 1.3 mm cars for "contaminants in common household products such as cosmetics, fabric softener and car polish that could cause a brakelight switch malfunction" vs faulty suspensions.

-

The competition for EVs is all cars, not just other EVs. The EVs that BYD makes aren't very competitive with Teslas. Probably more competitive with other downmarket ICEs. (and please, look at products vs products, not at a few specs on a piece of paper... that's the dumb way of comparing products that leads to people missing all the things that aren't easily quantifiable but that are important to customers) What's the secret sauce that Tesla has compared to some of the newer competitors like NIO, Li, Lucid? Because functionally and aesthetically the vehicles don't seem much different. Sure, but if you're (not you specifically) going to claim that there is some specific moat beyond performance metrics and luxury standards then the proof of burden is on you. So far the bull case has been "everything else is vaporware and everyone else is 5 years behind Tesla in battery function and engineering." That gap seems to be quickly closing as there is not multiple EV companies producing products with similar metrics on paper. What is the Tesla moat over the next five years? One risk to Tesla is that all their cars look alike. The S and X are declining in their production, and they are the ones with unique designs. Literally no differentiation between any 3 other that color. The Y looks like a 3 on dubs. I can't imagine this works to their advantage over the long term.

-

Agreed, I made the point more so because I think there's a very clear trend of underdelivering, and so it would seem logical to incorporate that into one's forecasts...

-

Also in that vein, it's fun to look back at certain other predictions that didn't pan out. If your 2010 master plan suggested an affordable car that ended up being the S, 15 years after the attached prediction you're not close to achieving a $25k car, how does one model future cash flows for this business?

-

I've been unbelievably wrong about TSLA, so I thought it'd be interesting to read through old posts. For as much consternation as this stock has created, what a prescient post from six years ago. Great reminder how narrative can drive many stocks for far longer than anyone would expect.

-

[Wolf of Wall Street style] I'm not leaving :-* [/Wolf of Wall Street style] It blows my mind that the fact that Tesla is the EV leader seems to give them in your book the right to lie about the solar roof product and autonomous driving. So let's make an analogy. Suppose NKLA was world class leader in hydrogen powered motor scooters. Would you consider the mockups and renders related to the truck to be less fraudulent than you consider them now? The world is more nuanced. People think "fraud" means it's a zero, when in reality fraud comes in many shades of gray. Obviously Tesla has made some impressive cars that are very real. Also, Musk has made many claims that are either blatant lies (solar tiles on the Desperate Housewife set to help push through the SolarCity merger) or very aggressive timelines that may or may not ever come to fruition (too many to cite). So at this point it seems unlikely Tesla is a zero, but it does beg the question of whether investors should adjust their expectations of his proclamations based on their probability of either being (a) ever realized or (b) realized on the time horizon he articulates.

-

Not until they add George Shultz to their board! Although I'm not sure what to think about Jeff Ubben's presence on their board.