influx

-

Posts

154 -

Joined

-

Last visited

influx's Achievements

")

Newbie (1/14)

0

Reputation

-

I am still holding. I am not selling, not yet. That 30% pop was interesting on a big volume. Today is less good, but still up. I am surprised, yeah. Probably a catch-up and. I am guessing somebody relatively big is trying to get in.

-

Options insanity - stupid "rich" skew in Apple and others

influx replied to aws's topic in Strategies

Hi Folks, Can you please share what do you use for options charting? What do you find the best or few of the best that you use on a regular basis? 1. comparing the option price vs the underlying 2. different expiries and behaviour 3. past vs present. past behaviour, etc. 4. and many more relevant data to overlay IBKR? Barchart? Etc -

What's the duration of the puts?

-

Where do you see the growth I am curious? I don't see any growth unless oil price recovers. But I did trade this two times with commons and options. Probably a better scenario is a slow but steady recovery to ensure they can get a steady fcf if possible. It was a good thing to see that they can still refinance, even though the interest is higher going forward. Probably not many options available. Wrong time to refinance.

-

Much like Berkshire, Baupost. I would think the dry powder is part of the convexity in an old fashion way Can you explain the convexity of holding dry powder like you're talking to someone who got C's in his Econ classes? Sorry, my bad. I meant when the market goes down, I either buy the beaten down equity or buy call options and you get convex exposure. I didn't mean convex per se, but convex relatively to a crisis event (liquidity is what is the problem, most of the time)

-

How do you track podcast guests by their full name? How do you setup an alert? Can you please share and tell what do you use?

-

Much like Berkshire, Baupost. I would think the dry powder is part of the convexity in an old fashion way

-

Hey, I hope you are well. And I've started wondering why is it so volatile? Why do you think it is? I am embracing it, I don't mind, I am just wondering what is it the cause if it is stable and growing? Maybe the assumption is incorrect (growing, stable, etc) or maybe we've got incorrect market perceptions ? Would love to hear more on this.

-

https://www.freightwaves.com/news/why-crude-tanker-collapse-could-be-long-and-painful

-

I was told VLCC Fixtures Android app is relatively good. Anyone has any experience? I think there might be a desktop app as well

-

Are you after the income or ? Why would you not buy PSXP?

-

Not really STNG related, but I've been following EURN for the past 5-6 months, looks to me as a dividend related cycle. But maybe wrong.

-

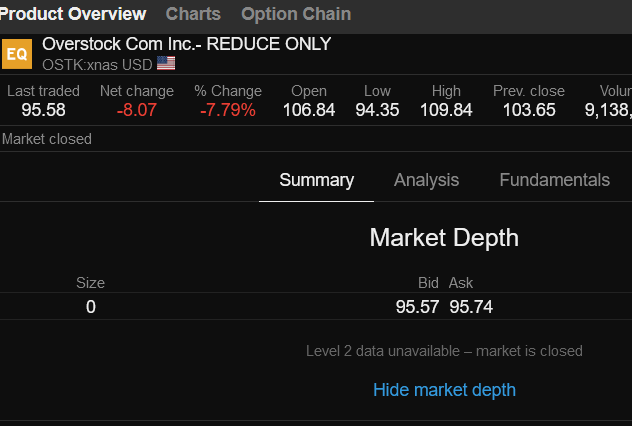

This has had a great run :) As of today one cannot buy via Saxo - it is reduce only. I am curious what do you guys see on your end?

-

Hi Guys and Ladies. I hope you are well. Is there a free screener/filter that I can use and setup. I'd like to use the default 52 week filter but modify the start and end date. Can you please help? Thanks

-

Yeah so it is the futures right? That's how I get 5 year leaps? Yeah, sorry, it is an old Grants article, 10 or more years, don't remember.