valuefinder0525

-

Posts

45 -

Joined

-

Last visited

valuefinder0525's Achievements

")

Newbie (1/14)

0

Reputation

-

"Baupost® posted high single-digit gains across all partnerships for the year ended December 31."

-

What Wells Fargo knew Exclusive documents show a Wells Fargo employee informed the bank of fake customer accounts in 2006 https://news.vice.com/story/wells-fargo-bank-scandal?cl=fp

-

The article makes me think about our industry (investing). It is much harder these days to find lasting businesses. There are a few other examples of these disruptors. Casper in mattresses Blue Nile in diamond rings Warby Parker in glasses

-

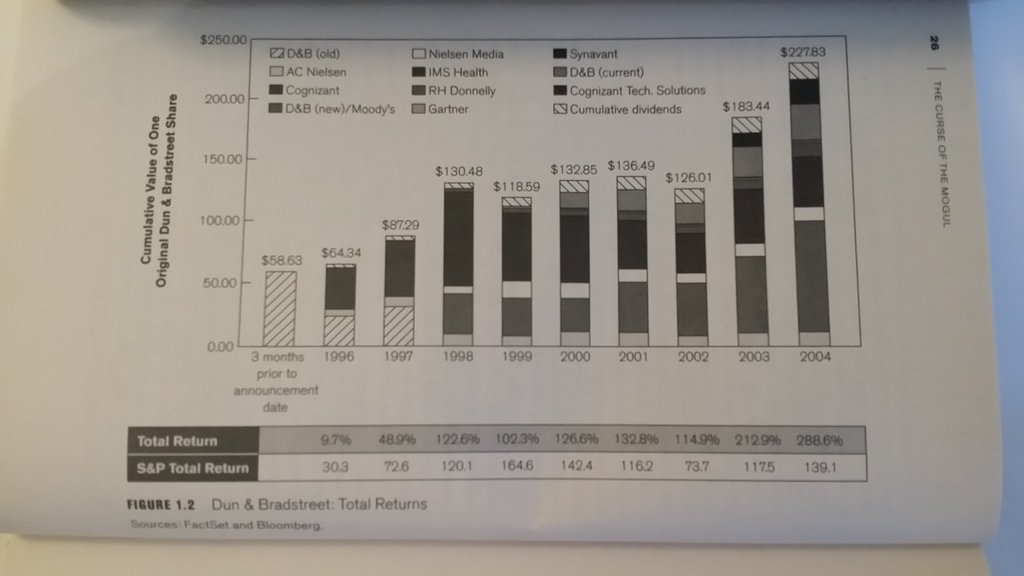

Amazing image of MCO's history

-

http://valueseekerinvestments.blogspot.com/2016/03/moodys-mco-vs-mcgraw-hill-financial.html

-

Hypothetically, let's say issuances and earnings were cut in half in 2017. You'd still be getting a 2.5% yield and would from that point certainly expect volume growth in excess of GDP on a go forward basis + pricing gains of 3-4%/year so probably 10%+ organic growth. So you'd be getting 12.5% returns on a go forward basis. In the short term you'd probably get crushed since your cost basis would be 40x earnings instead of 20x, and the multiple would come down, but in the long run, you'd probably do very well. Thanks for the color. In addition to my previous questions. I just want to get a better sense of what the incremental runway is for growth (and what the drivers are). How is the market getting bigger and how are MCO and SPGI getting a larger (or keeping) part of the market share.

-

How do you get comfort around future debt issuance? What if we are at record peak levels and it's a downfall from here? What are the drivers that allow you to get conviction around future debt issuance? MCO's margins are higher but the company margins seem much more volatile than S&P. Look at 2016 Q1, margins at hit with a decline in the topline. Speaking of 2016 guidance, do you still think they can hit it? It's looking less and less likely with all the Brexit volatility. The problem I have had in the past with these companies is that every time they look cheap, there is less conviction around the earnings.

-

Where is the next investment opportunity?

valuefinder0525 replied to jasonw1's topic in General Discussion

Does the author of that blog disclose his track-record (since-inception IRR)? I couldn't see it. No sure on the track record -

Have you done a brand by brand analysis in terms of the returns on the invested capital? Curious to see how many of the brands were good investments. Also any idea what Rupert could do with all the cash?

-

Where is the next investment opportunity?

valuefinder0525 replied to jasonw1's topic in General Discussion

https://oraclefromomaha.wordpress.com/2016/05/05/jd-com-a-multi-decade-compounder/ https://oraclefromomaha.wordpress.com/2016/06/13/a-response-to-the-jd-short-thesis-on-sumzero/ -

SH-HK stock connect http://www.hkex.com.hk/eng/market/sec_tradinfra/chinaconnect/Documents/List%20of%20Eligible%20Stocks%20for%20Northbound%20Trading%20(Eng).pdf

-

Moutai https://www.valueinvestorsclub.com/idea/Kweichow_Moutai_Co./138109

-

What are some of the research tools that people use in their investment process? A few that come to mind listed below: To check insider transactions http://openinsider.com/ To check executive salaries http://www.salary.com/Executive-Salaries/ To check political lobbying spending by companies https://www.opensecrets.org/ To check macro data points http://www.statista.com/ To screen for ideas http://finviz.com/ To check 13f filings http://www.dataroma.com/m/home.php

-

http://www.valuewalk.com/2016/05/kerrisdale-raises-100-million-short-dish-network/

-

Zhang Lei of Hillhouse Capital

valuefinder0525 replied to valuefinder0525's topic in General Discussion

Yes I completely agree with you. Many of his investments have been "creating the industry" around the particular company which he picks. It's truly amazing to have the ability and capital to do that.