Gregmal

-

Posts

6,429 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Gregmal

-

Trimmed some of the completely margined positions I have in WM and ARE.

-

I'd point out that dual agency is not even legal is some states(IE the best state in America...Florida, it is typically not permitted)....that said, Ive never had any issues...but I have my "people" and Ive used them regularly for the past decade and if there's a benefit to dual agency I am probably the one who is on the receiving end of it....as with anything, choose who you do business with wisely, and make sure they're intelligent enough to know where and how their bread gets butter.

-

Good catch, thanks...as I warned, dont trust anything I say! All aside, I think this is a one ft hurdle here. Its priced at a substantial discount regardless of how its broken down, its in a region that will continue to see tailwinds, and overall when you look across the RE spectrum, barring mismanagement(always a risk) I dont see many scenarios where other things do well and this doesnt. MF can probably be written conservatively at a 4.5 cap(what class B is going for currently), retail and office at 6.5-7 cap. Then throw in the "other stuff"....In this case, equity is worth north of $20 against roughly 4.6B in debt/preferred. If they get proactive or pull some levers upside only gets greater.

-

I also found it is a bit confusing, but not yugely material for the simple reason that much of the acceleration and rerating should occur as things clear up and if they proceed to do as they indicate, large swaths of preferred should begin disappearing, albeit not overnight but in a lumpy way like we just saw. Check the call where they basically said "we're in the market to buy, but when prices people were willing to pay accelerated, we pulled back and will remain disciplined".... the read through indicates to me they may make a couple sales... They've also, in a convoluted but eventually clear way kind of paired much of their assets in a way where you can match up each segment(at least thats how I view it) The MF nets out the entire stack of mortgages with a healthy positive balance. The office and retail pretty easily net preferreds. Cash+restricted plus loan portfolio goes straight to the bottom line. I grabbed the figure(looking at the notes I scrambled together) from the 1,631,646 additional paid in capital vs prior year 1,938,057 which looked to reflect redemptions(both forced from Series A call and investor requested). I didnt really include some of the smaller items such as cash and receivables(yes, lazy mans solution..guilty as charged) because I figured it would largely net out vs issuance/discrepancies resulting from my lack of patience sifting through the balance sheet with respect to preferreds in/on which changes every month, which itself seems to be getting netted to a much more scrupulous degree as Murphy mentioned on the call(re: comment regarding working with the B/Ds). Even if we see $100M net preferred issued less selling fees that money, should X out in terms of NAV left for shareholders on a forward basis....assuming all else equal.

-

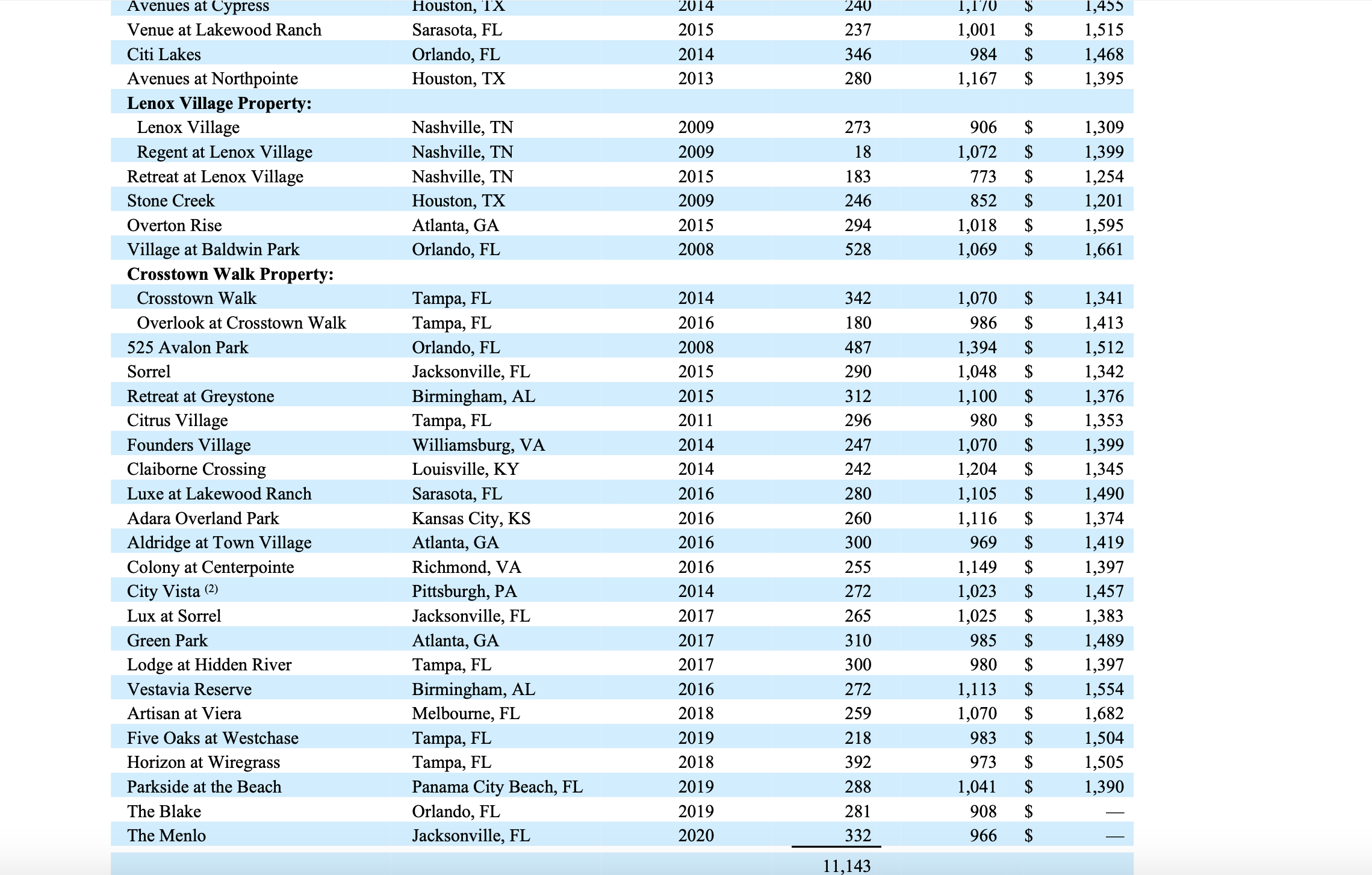

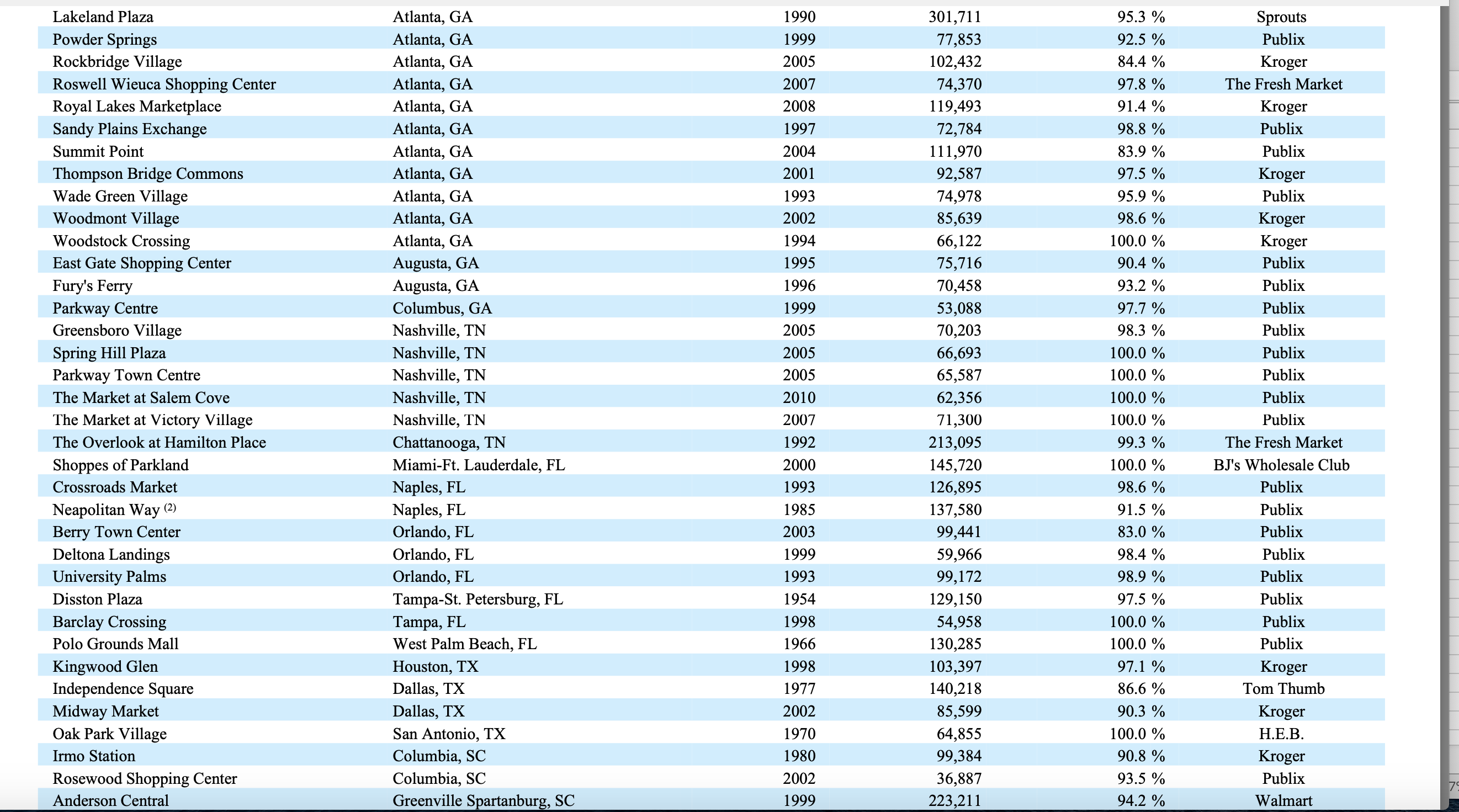

APTS $9.65 Company history Founded by legendary Atlanta developer John Williams. Williams, at 26 created Post Holdings which went on to be one of the most successful REITs in market history. He was pushed out in the early 2000s and the company was eventually sold to MAA. In 2009 he and his long time business partner started Preferred Apartment Communities. They took with them the Post model; beautiful, vibrant, class A multi family communities and a culture of excellence plus avid community involvement. The company went public in 2011 and by year end held $92M of assets which produced about $7M in revenues. At the start of 2020 APTS owned north of $5B in assets and was closing in on $500M in revenues. Whoa growth! Williams passed in 2018. Current management consists of CEO Joel Murphy; an industry vet with over 30 years experience who previously had been heading up his own firm and before that a long tenured executive at Cousins. He started off at top law firm King & Spalding. At CFO is John Isakson who worked with Williams the prior decade and also happens to be the son of former Georgia senator Johnny Isakson. Both I consider competent, and savvy industry vets who know the business well and possess enough discipline not to screw up my investment. Why its Cheap 2020 was not the year to undergo a major transformation if you were a small cap REIT with retail and office exposure as well as a funky capital stack and an external manager! Major changes occurred during the year; starting with internalizing the management…followed by the student housing portfolio sales and the decision to allow shareholders to vote on calling in the preferred shares at 5 years instead of 10. For these reasons and many others, the company screens like total dogshit. Makes total sense too. Valuation Sun Belt RE has been on fire. This was touched on very thoroughly on the recent YE call. As much as 50 bps compression and this after several industry reports put Q2/3 cap rates for similarly located MF assets in the low 4s! APTS portfolio is easily class A; most buildings have been purchased new, and within the past decade. There’s ~$135M NOI which yields a valuation between $2.4B if you assume its all “value add” stuff(for those less familiar with RE, value add basically means fixer upper crappola). If you value it as class B/C ~$2.85B, and if you value it as class A(why wouldn’t you? It’s the very definition of class A)…you get ~$3.4B….attached to these are about $1.4B in mortgages with more than 9 years average term, fixed and a mid 3s coupon. For the New Market portfolio, which is the company’s retail portfolio, owns almost exclusively grocery anchored class A shopping centers. ~20% of NOI comes from southern powerhouse Publix…with which Williams and Murphy both hold(or held) close relationships with from decades of work together as they in many cases grew together throughout the same regions. Publix is frequently signing new leases that spur PACs development pipeline. At an 8 cap on the retail(which is generally reserved for value add type stuff) you get ~$960M and at a 6 you get around $1.3B…attached to these is ~$600M in mortgage debt, fixed, at a hair under 4% with more than 7 years remaining, on average. Preferred Office is the final segment of significance and again features almost exclusively, class A office, 95% leased with predominantly investment grade tenants and an average remaining lease term north of 7 years and 1/3 or so going out into the 2030s. At an 8 cap you get an even $1B valuation and at a 6 you get a bit north of $1.3B. Attached are $633M in mortgages, fixed rate a hair over 4%, and average length of maturity over 12 years! Taking the whole enchilada you can see a very clear value range between 4.36B assuming what they own is on par with Canadian Goose droppings in Central Park and on the more realistic, but still not stretched side of things…roughly $6B in FMV/NAV. Other issues of importance…there are two. Financing…which the company describes as: consists of the Company's portfolio of real estate loans, bridge loans, and other instruments deployed by the Company to partially finance the development, construction, and prestabilization carrying costs of new multifamily communities and other real estate and real estate related assets. There are about $320M in face value loans. These produced ~$50M in revenue last year. Average rates are low to mid teens. Traditionally, this has been a big time revenue generator for the company. Not just because the loans are asset backed and typically good….but because this is largely how the company funds its acquisition pipeline. They find interesting land or projects. They then put up the money for development in the form of a loan and included in this are a purchase option for the finished product. This does not mean they always convert…fairly often they sell the loan or simply decline purchase option and receive their proceeds plus interest when the entity is ready to be monetized. But in general, this unique process has been a way to cultivate relationships…of which they have more in their core Sun Belt markets than any other company I am aware of….and additionally locks in building relationships with other developers which can and does benefit future projects. Preferred shares This is the big one. The primary reason all the two bit book reporters on places like Seeking Alpha hate PAC…the preferreds! Its why even Brad Thomas’s Jim Cramer like summarizations of REITs land APTS in the “lemon” category. But context is key to everything. This company, as was mentioned earlier, started with nothing. Anyone familiar with the REIT world knows that subscale REITs simply cant raise capital….or if they do, its very expensive. So…how do you? You have a genius like Williams who knows a thing or two about the dastardly non traded REIT markets which have swallowed whole many stupid, yield hungry retail investors. Except over the years, FINRA/SEC have started frowning upon these issuances or making them much more difficult….except…what if you aren’t issuing shares of a non traded REIT? Afterall, its “non traded preferred stock!”….totally kosher and fine and because PAC is public…all the better! Issuing these shares in the public markets would not only be more expensive, it would also be impossible as PAC has ongoing broker dealer selling relationships that effectively allow them to raise capital AT WILL! The cost? 6-7% coupons and about a 7% commission to the agents….all in all, a bit expensive, but hardly anything outrageous if you considered the alternatives. Then consider the fact that these preferred basically have no say in anything and only a liquidation preference! To boot, you have incredibly harsh early redemption penalties…up to 12% for the first year…. And the company has the option to settle in cash or stock. Soooo….access to capital with no/little restrictions or covenants, at will, and a 6% coupon? Pretty darn creative and good to me… or so I think. Now flip things a bit and realize that many of the properties they are buying, net this out entirely….so the equation effectively looks like this….Preferred shares get the income, common gets the growth for free. Hardly worth all the tears every simpleton taking a look at this thing over the years has shed over “oh poo poo the preferred take all the economic benefits! Wah”….NOT TRUE. Besides, who cares about the dividend in the current REIT environment? ESRT cut its dividends and promptly doubled within several months last fall/winter. When value dislocation is this significant, focus on what really matters..which isnt a nickel or dime a quarter. Anyway..the company has about $1.6B of these bad boys outstanding. Proof? Do you need proof that if you loaded the boat on Sun Belt RE the past decade that you’ve done well? Probably not, but look no further than the company's recent sale of Avenues at Creekside….boom. Going into 2021, the objectives are clear. Listen to the Q4 YE call. Murphy is on point. These guys are focused. They’ve already backed off pipeline acquisitions as cap rates have compressed. Read between the lines. The narrative shift happened and on top of all this you have extremely favorable, covid enhanced NTM comps….Back out what you wish but the guidance on FFO covers what they need it to and that leaves you with a NAV range of $10 on the assumption that Class A is priced at “value add or worse”… or ~$43 per share assuming its priced as the current private market comps indicate….or somewhere in between? Who knows? Also add in the favorable upside, as I previously mentioned….that roughly every 10% increase in the portfolio value translate to $10 per share of NAV being created. Why is this go time? Because everything has been set in motion and the company has practically told shareholders what they intend to do. They’ve started doing it already. And it makes sense because the company has reached scale and once the preferreds are out of the equation there is little reason they could not then tap the capital markets the way traditional high quality REITS can. Will probably have more….threw this slop together because its been a popular idea and I’m sure if nothing else it will help folks hone in on whatever it is they are looking for to either support or discredit the thesis. Disclosure: Don’t ever trust a word I say and assume I am trading against you. I probably wont be….but your investment decisions or your own, not mine. Be responsible. I am actively purchasing shares in this name today, 3/22 and expect to continue to do so. Cheers

-

https://www.coindesk.com/judge-in-sec-case-drops-bombshells-that-are-positive-for-ripple-xrp-says-lawyer That and Tetragons garbage suit was laughed at https://www.financemagnates.com/cryptocurrency/news/tetragon-lost-case-to-reclaim-175-million-ripple-investment/

-

AIV- Apartment Investment and Management Company

Gregmal replied to CorpRaider's topic in Investment Ideas

Yea whats also interesting to consider is that the spin off date was Dec 15. Per security law, blackouts are required to occur 2 weeks prior to quarter end and cease 2 days following the earnings release. So the first opportunity he had to buy he bought 100k shares. And following up, he's bought 100k shares every day he's legally been permitted to do so. And, he dropped the filing late on a Friday after the close which mean he wants to keep it on the DL.....so draw your own conclusions. Mine, stunted in disclosure mainly because I was both away and unable to post for a month and a half or so is that...the two biggest risks here IMO are gone. Democrats control congress and bailout money is already heading to blue states. Conditions will become significantly more favorable for NY/CA etc. You won't have to worry about unpaid rents. This will also produce some sort of inflation..which by itself should almost certainly make Parkmerced and those beautifully located 150 acres good enough to get par on the mezzanine loan. That loan is ~$2 per share. We're seeing record prices for office and retail RE assets so I think its time people in the public markets stopped mandating a 50% haircut to these type of assets. -

AIV- Apartment Investment and Management Company

Gregmal replied to CorpRaider's topic in Investment Ideas

Mr. Considine must have gotten word Gregmal was buying last week. -

Quite an impressive inventory of properties. The management internalization expense makes things look horrible until you look at the potential savings going forward. I put green arrows next to the lines that I assume represent the savings (see attachment). I'm also assuming the $180m expense closed the deal. Thanks, I'm in. Yup, the internalization of the manager and the student housing sale were the big ones last year thats seemed to indicate a fundamental shift...both planned before the pandemic even began, rather than being a result of it or anything perceived to be out of desperation. The last call talks a bit about the focus going forward, on fixing up the issues around the capital structure which leaves nothing other than to assume they plan to possibly get rid of more of the preferred, or if nothing else, slow down the pace of issuance. It's Friday after the close so Im wrapping shit up for the week and Ill get into it at a later point, but the preferred were brilliant for what they allowed the company to do and capitalized on a great regulatory loophole...but getting those wound down would greatly benefit existing shareholders. My only caveat, which didnt stop me from buying, and won't stop me from continuing to do so...is management. Things are a little convoluted because we had the external manager issue prior...but if you were a holder of the common pre 2021...and especially pre 2020, it seemed as if there was a growth at all costs/kingdom builder mentality....only problem(or benefit if you are buying now) is that they basically bought stuff that was good if not great, and now just turned into gold because of the pandemic. So they got lucky in terms of emphasizing growth and being focused on the right dirt. Could have just as easily been buying properties in NY/CA etc....moving forward, the signal I get from the moves made in 2020 and the recent call, is that theyre going to be more selective and a little bit more skewed towards getting the common back to a level that makes sense. Some of the preferred issues have warrants or conversion features in the high teens and around $20(none are publicly traded unfortunately)...I also think theres some alignment within the compensation structutre....it is predicated on a TSR and peer group outperformance rather than just buy more sq/ft or whatever. Further, just roughly speaking, you have tremendous leverage to upside. Probably trades conservatively at a 50% discount to NAV and every 10% increase in the portfolio translates to roughly $10 per share on the common. A lot has to go wrong/really, really blow up for things to go poorly at the current price. More than half the asset value is in multifamily. And if you want an idea how undervalued that portfolio is, look at the Creekside sale that took place not long ago.

-

Definitely in the news a bit recently. You had the unfortunate death of the young child, and then this... https://www.telegraph.co.uk/news/2021/03/19/joe-biden-trips-stumbles-three-times-boarding-air-force-one/ "Mr. Biden, who has said he uses a Peloton bike to keep fit, often makes a point of jogging in a show of his fitness" Hopefully PTON launches a stairmaster soon.

-

I looked at both S-1 and I can come to terms with CPNG but what is really OSCR bus8 es model, is it like LMND for health insurance. Their numbers look atrocious. Both GOOG health care IPO‘s AMWL and OSCR look underwhelming to me. I havent even come close to a deep dive, and yea, the approach is at best scattershot, but the impression I have gotten is that somewhat like LMND, theyre focusing on developing the brand. Its not very efficiently rolled out, but they have a little bit of everything...their own clinics, the tele health offering, pricing models that "appear' transparent and are generally received well by their customers. My guess is that they would be burning many times more money if they put all of this into motion in all their markets, all at once. All in all I think its probably burned through a good bit of money experimenting and will continue to do so. At the same time trying a lot of things in a scattershot way sort of lets you feel out the sensitivities of what works and what doesnt. Its in the right place at perhaps the right time....there does seem to be bipartisan support for fixing a lot of the issues in healthcare....so you'll need to cross a few bridges to get there, but there are bridges which lead this to being a bit of a disruptor. At the least its a small starter that will compel me to do a bit more work on it while the market is beating the shit out of companies like this...and if nothing else I'll probably be able to unload it later once things settle down. $32 was the original low point of the IPO range that ended up being revised upwards twice to $39. So I'll take my chances there.

-

Peloton was a $30 stock pre covid. Its a tough argument to make that the company was destined for greatness before the pandemic. Its basically the poster child for stay at home/covid plays; perhaps only outdone by Zoom. Ive got puts on a basket of stuff like this and individually its not a meaningful or high conviction idea, but if you're long, I think theres much easier ways to make money. You're not long youve said so I am not sure where your bread gets buttered either way, unless I am missing something. And if Q2/Q3/Q4 '21 sales are up 30% year over year, that would be a pretty remarkable feat.

-

TPL at the close.

-

Good volume and follow up to yesterday's big block trade. Perhaps thats the last of Par. Been running around doing errands all day and trying to work as little as possible because then I get to claim a ridiculous by the hour wage! So the real answer is, I dont know.... that said this is exactly what you wanna own in an inflationary environment. Winners gonna win.

-

Took a wee little starter in OSCR and CPNG.

-

Yea I'm not hating on everyone in the field...but the truth is that too many finance folks are too full of themselves(or just in general take themselves way too seriously) and many think they are hot shit because of how much money they make, but the truth is they dont deserve to make the money they do and its not hard doing what they do. Look at this guy Keith....chills in his basement and has fun with it. Plenty of others have mentioned similar things...I think(although I wasnt around for those days) ERICOPOLY even talked about how he'd spend some time researching and then just go for walks on the beach...I cant say I do things much differently. Its a shame folks just dont know any better and therein lies the problem.....the system is setup so that people are not properly educated in matters relating to financial markets and investing. And I can take some good guesses as to why that is....

-

Well duh! The CFAs, MBAs, CFPs are just marketing gimmicks. One of my good friends is a CFA. Some years back when he was training I asked him what he was so focused on. He said he's working on the 2nd test. I laughed and jokingly told him he's one of the worst investors Ive ever met....if he got the designation, it would just be misleading to people who didnt know any better! He goes "yea but I can make more money with it"....aint that the truth. My younger brother took level 1 and 2 of the CFA exams while in Med School. He's a bit of a math nerd and he did it for fun. Said it was a total waste of time. Folks love pitching "long term" investment strategies....because "long term" generates more fees than short term....

-

Total boss....Another example of how NOT HARD it is being in the finance biz. Anyone managing money making more than $150k a year is grossly overpaid in relation to the work they do. Myself included!

-

Its kind of hilarious in a warped way how the answer in regards to pretty much every social/economic issue is that it benefits the rich....Darwinism is inevitable. Unfortunately. Oh your phone bill went up 8%? Ah, I made some good money on my telcos last year! Oh rent went up a lot? Yea my MF reits were raining cash on me all year! $4 gas? Did I say I owned TPL?

-

Ok so let s try to lay out whats going on here... Yesterday I highlighted a post from Dalal in December touting index inclusion and also stating "still waiting". Dalal said he wasnt "cheerleading" although going through the thread, thats debatable. Also, nothing wrong with cheerleading or being excited about an investment...Perhaps we can just agree to disagree in terms of the adjectives being used. Nevertheless... "still waiting" was Dalal for the fad thesis to be proven....a mere 2 weeks from his previous post. I am not certain what experience one has with fad based investments, but if in that 2 week window you were expecting the fad thesis to be disproven....thats pretty elementary. The time line has been laid out several times, by several different people. Coming in every two weeks or two months while many places are STILL on lockdowns or facing severe state induced covid related restrictions....not sure what you're not understanding or trying to accomplish... You are also now claiming that current sales and backlogs are not covid enhanced....not even sure how to respond to that. Also, you are now calling insider sales, "thesis creep". I am not sure if you understand the term thesis creep if discussing insider sales is something you think adds to the bull case. Its important because insiders obviously find selling at these prices attractive. Not to mention you dont find the stock worth owning either, evidenced by the fact that you sold it. Similar to Tesla, you made a nice "trade"....you made money. Good for you. But dont be like the people you mock such as Andrew Left/Citron and trade momentum while touting fundamentals...You sold Tesla at $800 pre split and continue to roam the thread mocking people. Now you're doing the same here.

-

Admittedly its not cheap, but the best companies rarely are. Plugging 40%+ growth rate into the Gordon growth model doesn't exactly work either on this one d/[k-g] I was listening to an old Peter Thiel speech on his biggest mistakes. he said not investing in series B at facebook. He had led the series a for $500k at $5mm valuation, and less than a year later the B was implying $98mm (the company was still pre revenue). something he pointed out that I think is true, companies with high momentum will have these quantum leaps in growth are often the most undervalued because people have a hard time justifying their staggering valuation levels. My biggest mistakes in investing came when I as younger trying to view everything from the traditional valuation lens and avoiding tech companies simply because Buffett historically did. I'll start off by saying that PLTR has been around for two decades now, so they arent exactly the new kid on the block. Otherwise, you are ahead of the game if you are cognizant of the rest of what you wrote. The best educations are first hand, but you can learn nearly as much by watching and listening to others. Both in terms of what they do well, and what they dont. And yea, Buffett is the GOAT, but he's also not exactly the end all be all. I recall a number of folks here refusing to invest in the market last spring because "Buffett was bearish"....Buffett also said Bitcoin was rat poison at $5,000...its fine to be inspired by others but thinking for oneself is crucial to successful investing.

-

Speaking of competition...LOL/ Is Sanjeev short this?

-

Exactly. Christmas 2020 was basically a "hey look at my Peloton, did you get one too?" fest....its a product of environment and circumstance. And I would be hard pressed to believe this continues. Behaviors of the masses are fairly consistent and predictable. Working out is not a national pastime in the land in which 40% of people are obese. And while one could make the case that they should make working out more of a priority....they never have and they probably never will. I would love to see their sales breakdowns by region as well. I can probably guess where they have the best sales. And on top of that, those regions often have delusions of grandeur regarding themselves and their extrapolations in respect to the rest of the country/world can be quite jaded. Before I spent a couple months traveling I had various conversions with a bunch of friends and contacts...almost all of whom are in the investment business out of NY/NJ/Connecticut. I've also spoken with most of them upon returning. And all I can say is the majority of these people have no idea how things are outside of their little NY-centric bubble.

-

To be fair, if we're talking about the fundamentals, here you were cheerleading an index inclusion as evidence this isnt a fad.....and most of your "this isnt a fad" proof is confined to a period spanning less than 12 months. I think the most reasonable assessment was that numbers would top out in Q1(or more loosely December 2020-March 2021) or so, and then comps would then get very tough. Only time will tell on that. Not analysts upgrades/downgrades or "research reports"...Perhaps one day it can be an excellent, cult like brand...... with a $12B market cap!

-

Yup, yup. Meanwhile the uninformed are focusing on whether they can cover the dividend or not and how come the release showed they lost money last year!! Try plugging in modest price appreciation on Sun Belt assets and see what that does to the equation! Actually just try marking the current portfolio to market instead of gross reported GAAP based asset value...