adhital

-

Posts

74 -

Joined

-

Last visited

adhital's Achievements

")

Newbie (1/14)

0

Reputation

-

https://www.barrons.com/articles/how-to-value-bill-ackmans-spac-deal-the-sum-of-the-3-parts-implies-30-upside-51622833744

-

why so, if I may ask? ebitda is coming out straight from income statement. They capitalize content spend once and now expensing (or depreciating) it for some number of years. but yes, to compare apples to apples across content producers vs. content purchaser is to adjust the accounting. such as, capitalizing content related expenses for producers as well. Looks like EBIDTA margin is 30% for newco vs. 60% for netflix, perhaps for the same reason.

-

well.. we've another comp for fun! "Amazon.com Inc. AMZN 1.54% is nearing a deal to buy the Hollywood studio MGM Holdings for almost $9 billion" = 9x 2020 Rev or. 65xEBIDTA https://www.wsj.com/articles/amazon-nears-deal-to-buy-hollywood-studio-mgm-11621880759?mod=hp_lead_pos1

-

(I think this should go to Netflix thread.. apologies to COBF members) @SpekulatiusIs it 33x EBIDTA against a market cap (equity) Or, EV to EBITDA? I got the original number from Interactive broker's ratio value for Netflix. Just for fun, I spend 15 min using https://s22.q4cdn.com/959853165/files/doc_financials/2021/q1/Q1'21-Website-Financials.xlsx, but please correct me if not the case as LM helped me on the DISC data ? Total Diluted share count 455mm. market cap 455 * $504/share = $229 B EV = $229 + $15 - $9 = $235B. LTM: EBITDA = $3.73 (Net Income) + $11 (Amortization of content assets) + $1.58 (Depreciation, Interest and Taxes) = $16 B EV/EBITDA = 235/16 = 14.68 The heavy item here is the amortization of content assets. It is $11B LTM as most of the content is licensed and amortized, unlike TW or DISC original contents spending. This is why EBITDA comparison may not be of much help

-

good catch. I was comparing EBITDA against equity vs EV like you're doing. but yes, I need to add additional pref conversions and the ratio becomes 6 at today's EBIDTA, still below comps but not as cheap as I thought. ATT paid 12.6x 2016EBITDA for TW . In comparison, Netflix EV is 14xEBTIDA I think...and we're paying 11x for newco. Doesn't looks like a bargain but need to dig deeper into accounting for a precise EV/EBITDA comparison. (I think you may need to take out cash and cash equivalent to get precise EV but I don't think it matters much though)

-

@LearningMachine It was a simple math but I may of way off here so please correct me. "Upon consummation of the Merger, existing shareholders of Discovery will own approximately 29% of the outstanding shares of Discovery on a fully diluted basis (computed using the treasury stock method)." "~$52B of expected revenue and ~$14B of expected adjusted EBITDA in 2023" newco 2023 adj ebitda = $14B. 29% belongs to the current shareholder ~$4B or current discovery is selling at (based on $32/share) ~4x of $4B Capital structure and cost accounting for contents (amortization schedule of content license vs original shows , vs opex spending on cable etc.) are different for TW, DISC, Netflix. ebitda comparison is not ideal but still valuable IMO

-

someone criticized revenue multiple valuation as too simple.. at the end of the day, revenue is what matters; however, I’ll welcome another criticism Buying disca at the current price is like paying ~4x adj ebitda for newco. T bought TW for around ~10x. Netflix is selling at ~12x 2021 ebitda. TW was selling for ~8x ebitda when it was bought by T I don’t mean that this is the only parameter to look for and jump in.

-

Their yearly combined revenue is almost twice that of Netflix and all the $$ they are now spending on buyback and dividend payout plus $3B cost savings will go towards contents. So they’ve the fire power. May be they should start bundling it now rather then waiting for official merger next year.. who knows they might announce something soon

-

I think at the end of the day, TW/D is competing with Netflix audience ultimately. No one is going to switch prime, that’s for sure. Disney is on its own. I won’t be paying for both as well given YouTube and prime options. I read it somewhere that GOT is getting renewed for few seasons. Also, WB pictures likely to be played on this platform pre-release... If they offer, say, $15/month for whole package plus additional income from cable advertising, I think they’ve a shot..

-

Yes, I’ll pay for YouTube as well. But, HBO is not bad too.. I’ve both Netflix and hbo and I think I spend equal time watching both but I think I like hbo better though.. and now Combined with news, TLC, food etc.. I think the package would be compelling for someone to switch.. that’s why poll would be interesting. Twitter might be of help here ?

-

@Spekulatius how much would you be willing to pay (or ditch Netflix) for TW/Discovery contents? ad-free and ad supported versions for example? Don’t know how to setup a poll here but would be interesting to know

-

@LearningMachine I think the main issue we have is that GMV is not a defined accounting term and the numbers are unaudited. In the absence of accounting rules, Alibaba or JD or any companies are allowed to define GMV as it chooses

-

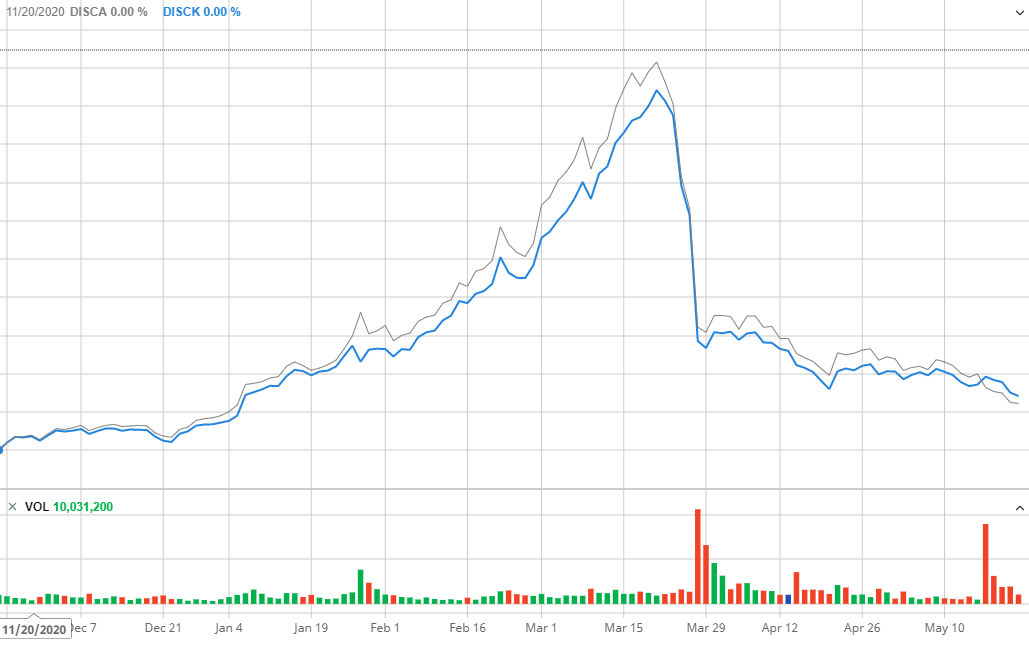

based on this chart, looks like shorting DISCK and buying DISCA is better buy ?

-

Sorry that’s a silly argument ?

-

Zaslav options are currently trading out of the money with about half of them vesting in May 2026 and in 2027. It need to rise above $36/share for him to make money. Regarding valuation, Netflix has compounded revenue by over 25% since past 10 years and trading at around 8x revenue. Is it expensive? I don’t know but it's not cheap either. Discovery has compounded revenue by just over 12% during the same time frame. So they’ve created value but I don’t think trading it just around 1.5x is fair. If the merger goes through and if they can improve the revenue growth and margin expansion in par with netflix, this should get rerated substantially. $3B synergy can go towards content spending. FCF may not be way to value this going forward given the capex it needs to invest on contents. Netflix is spending $18B just this year with $25 annual revenue. Discovery/TW likely will spend on the same ballpark. If they can pull off the margin expansion, smart capex spend and gain market share , its not very hard to imagine the combined company to trade at least 2x forward revenue, if not more. Just based on this simple math, 2023 fair equity value can be > $100B or 30B for Discovery shareholder. We can discount back to PV using whatever discount rate we like to use, but the current share price cheap. It’s at least double from here in next 5 years Or, could go much much higher. Taking debt improvs the ROE too. I sold it a while back and have started buying. downside is not much either if the merger don't go through..