nwoodman

-

Posts

310 -

Joined

-

Last visited

1 Follower

nwoodman's Achievements

")

Newbie (1/14)

0

Reputation

-

https://www.wsj.com/articles/berkshire-hathaway-to-buy-500-million-stake-in-brazils-nubank-11623153600 Brazil’s digital bank operator Nu Pagamentos SA said Berkshire Hathaway Inc. BRK.B -1.05% agreed to buy $500 million of its shares, as digital banking expands quickly in Latin America’s largest economy. The investment is accompanied by another, $250 million deal that includes various domestic and foreign investors, Nu said. Both deals were signed late Friday and put the company’s value at $30 billion, Nu said. The São Paulo-based, privately held firm operates via its Nubank brand. It is the largest fintech in Latin America and one of the largest in the world, with 40 million users in Brazil, Mexico and Colombia, the company said. It has raised around $2 billion since its inception in 2013, Nu said. The company said Berkshire’s is the largest single investment it has ever received. Nu didn’t disclose the size of any investor’s stake. Todd Combs?

-

Some very sensible observations regarding a lock in but I do hope you are wrong. Jump Prem!. Arch, 1 thousand, 2 thousand, 3 thousand……

-

More USAP. Not difficult to see a decent ramp in aero as things return to post covid normal. Price target simply book of $20+. Operational leverage is the key https://www.thestreet.com/investing/boeing-general-electric-leap-as-airbus-boosts-production-targets

-

USAP

-

FFH

-

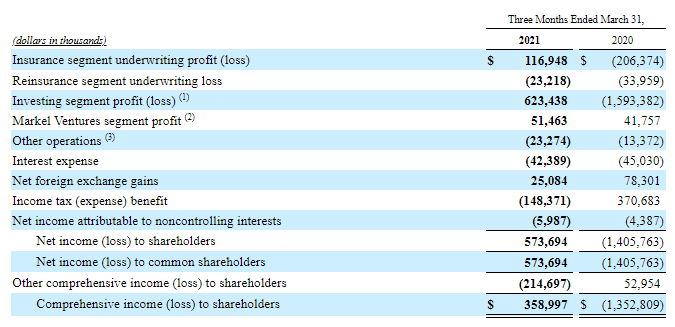

Q1 Results out. Markel Corp - Markel Reports 2021 First Quarter Results Highlights of results from the quarter include: Earned premiums grew 13% in 2021, reflecting continued growth in gross premium volume from new business and more favorable rates. The combined ratio for the first quarter of 2021 was 94%, which included $64.3 million, or four points, of net losses and loss adjustment expenses from Winter Storm Uri and $18.6 million, or one point, of net losses and loss adjustment expenses resulting from an increase in our estimate of ultimate losses and loss adjustment expenses attributed to COVID-19. The combined ratio for the first quarter of 2020 included $325.0 million, or 24 points, of net losses and loss adjustment expenses attributed to COVID-19. Excluding these losses attributed to Winter Storm Uri and COVID-19, the 2021 combined ratio reflected meaningful improvement in both our current accident year loss ratio and our expense ratio compared to the first quarter of last year. Net investment gains in 2021 reflected an increase in the fair value of our equity portfolio driven by favorable market value movement. Net investment losses in 2020 reflected a decline in the fair value of our equity portfolio at the onset of the COVID-19 pandemic. Operating revenues from our Markel Ventures operations in the first quarter of 2021 included significant contributions from Lansing Building Products, which was acquired in the second quarter of 2020. Comprehensive income to shareholders for the first quarter of 2021 reflects the contribution of net income, partially offset by decreases in net unrealized gains on our fixed maturity portfolio resulting from increases in interest rates.

-

Thank-you. Watched it yesterday and found it inspiring and frustrating at the same time. Read your transcription today and got twice as much from it in a tenth of the time. Great work Matt!

-

+1 although purchase was via HKSE (9988.HK)

-

Morgan Stanley are out with a long form primer on India. A good read over a morning coffee. The work Fairfax has put into establishing their “hunting license” should really start to pay off over the coming years. india_20210405_0000.pdf

-

Great question. BRK (50%) FFH(30%) AAPL (20%). Berkshire will likely provide acceptable returns from this point, especially with buybacks now a meaningful opportunity fo capital allocation. Fairfax makes the list for me for providing an emerging market basket, in particular India Apple, if health turns out to be their “greatest contribution to mankind” then they deserve a place. Lower % because of exposure via Berkshire

-

Thanks VIking. Even with a most remarkable re-valuation of their major holdings, there is still a modest discount to fair value. It is going to be interesting to see the price they retire the swaps on themselves. My guess would be around USD600/CAD750 per share, P/B~1.2

-

In cricket mad India, having Virat Kohli, the captain of the national team, as “the face your company” makes good sense to me. A personal investment in Digit by Kohli should make him a most enthusiastic advocate ? https://bestmediainfo.com/2021/04/virat-kohli-joins-hands-with-digit-insurance-to-spread-awareness-about-insurance/ Kohli invested $340,000 back in early 2020 https://inshorts.com/en/news/virat-kohli-anushka-sharma-invest-₹25-cr-in-startup-digit-insurance-1582106868622 https://economictimes.indiatimes.com/small-biz/startups/newsbuzz/virat-kohli-anushka-sharma-invest-in-prem-watsa-backed-digit-insurance/articleshow/74197271.cms?from=mdr

-

Great quarter and the tailwinds seem to be growing. MS maintains their target of $105, this is roughly where I have them pegged too. That GM forecast of 40+% is pretty amazing though. MS take: We continue to see relative value in the stock: Micron's trough earnings power surprised us, and should bode well for longer term value creation. In the last few quarters, we have been surprised at the resiliency in Micron's gross margins, given the sharp compression in PC and server DRAM. The company's success in graphics DRAM, at improving the mobile mix towards DRAM+NAND modules, and in embedded DRAM, has driven this outcome. As a result, despite numerous substantial challenges, the company was able to earn about $3 in EPS in a difficult FY20 and FY21. As conditions now look to be bottoming out, we would characterize that as trough earnings. While we're not sure we will see EPS back at new highs of $12 plus, if we enter into a phase of improvement, that is where we expect sentiment will quickly go, leading to through cycle earnings potential of $7.40 or so. Given the rerating in the semiconductor space over the last 24 months, we see substantial relative value here. Our price target remains 14.5x that through cycle number (a discount to the group given higher cyclicality and lower free cash flow yield); that leaves our target at $105, and we remain OW the stock. MICRON_20210401_0000.pdf

-

A rational observation and one that I think about far too often. This company is the epitome of ‘the call of the value sirens” at times. I think the individual IQs are high but something happens on occasions that leads to a Dunning-Krueger case study. I agree with many that put it down to the opioid hit that was the CDS win following the 2008 housing bust. Hubris, ego?not sure but it all starts and ends at the top. Mini rant out of the way, there is a base that has been built that is pretty amazing. That too can be attributed to senior management. I know hope is not a strategy but I do hope that with a hard market, they make some money, deleverage and lower their expectations. The market has already lowered its expectations to a point where investors from this price point should do somewhere between OK to good. The caveat is will Fairfax stop “being clever’ and look for 1ft hurdles. I personally feel that they have their ducks in a row - Insurance, Atlas (offloading APR is enough, do nothing) and India. Just concentrate on these, execute well and all will work out fine. Get distracted on “being too smart” and it will be another lost decade.

-

The highlight of the letter for me was that they are pulling out all stops to have Charlie alongside Warren for the AGM. Watching the DJCO AGM ( ), the diminishment in capacity at 97 is negligible. Truly amazing. The buybacks and tone only reaffirmed my view that Berkshire can be a cornerstone for my portfolio (10% +/- opportunities) and means that retirement is a possibility :). As always appreciate everyone's very thoughtful comments