giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by giofranchi

-

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Yes! But not as overpriced as fcf might suggest! Costs related to the acquisition and integration of new businesses are real cash outflows, and cannot be added back in calculating cash from operations. Yet, they indisputably are one time charges. And they might sometimes be as large as the amortization of goodwill, which instead is rightly added back. Gio -

Ok! Thank you! :) Gio

-

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Thank you for posting… but very bad article! It is Cash EPS which adjust for integration costs and other expenses related to the acquisition of external businesses. Imo it is Cash EPS that should be compared to VRX share price. A “financialized pharmaceutical company”? Just because it purchases products already developed by someone else, which have long life cycles and require little more spending in R&D? Mmm… Call it as you prefer, it remains a business model I like! If some synergies might be found and exploited, I like it even more. Sorry to say this, but I have come to expect much more from Mr. Grant… In the end, either Mr. Pearson is buying good quality assets cheaply, or he isn’t. If you are a bear on VRX, show me why Mr. Pearson overpaid for poor quality assets. ;) Gio -

It's not a particular number. It's what would happen at any given point in time if all warrants and related options were exercised. The bottom line for that calculation is the FDBV/S or the closely related FCBV/SH number that they report conservatively each quarter, rather than merely increases in BV/SH. It's what would happen if those vested securities were exercised instantaneously, considering the stock price at that time and the strike price ($5.00/SH for the great majority which expire in less than two years). The large number outstanding until then is mostly related to what sponsors got at their IPO, not management overreaching. :) Ok! But I am trying to understand something I found in the Westhouse latest report on LRE: Total PTP for FY2013 is $218.1 million, and Diluted EPS are $1.17. Then, they estimate Total PTP for FY2014 of $247.1 million, and Diluted EPS of $1.11. The only possible explanation to this “riddle” is that diluted shares outstanding in FY2014 will be much larger than they were in FY2013… Yet, at year end 2013 all new shares to acquire Cathedral had already been issued… Probably they used an “average diluted shares outstanding” for FY2013. But I cannot find that number, nor the number to use for FY2014… Gio

-

twacowfca, I am having difficulties to find the number of diluted shares outstanding… where can I find that number? ??? Thank you! Gio

-

Yes! You are right! A ROE of 25% is too optimistic! My point was that 3 years of subpar results might happen to anyone. Even to Mr. Klarman or Mr. Brindle. But who knows?! Mr. Brindle has often said “we create our own hard market”, and right now high-yield debt is not a very attractive market, but Mr. Klarman has repeatedly shown to be able to swim against the tide, hasn’t he? Therefore, I am never comfortable thinking I can outsmart great entrepreneurs and capital allocators… Hey! If I could stay with them only when they outperform, and stay away from them when they underperform, I would probably be richer and more successful than Mr. Klarman and Mr. Brindle!! ;) Keep it easy: find great entrepreneurs and partner with them at fair prices. I guess it is difficult enough! ;D Gio

-

I continue to believe it is dangerous to value an asset with a duration of 50 years or more on the basis of last 3 years results. Think of it this way: Mr. Brindle is among the best in the world in what he does, Mr. Klarman is among the best in the world in what he does. Mr. Brindle looks for the best bargains in global insurance and reinsurance markets, Mr. Klarman looks for the best bargains in global equity and distressed debt markets. Just because Mr. Klarman suffers 2 or 3 years of subpar performance, would you then infer that he is destined from now on to underperform? Or would you think more likely that his average performance in time will be more or less like the one he has experienced during the last 20 years? Or, put differently, why disregard the possibility that 3 years of underperformance might be followed by 3 years of outperformance? Mr. Brindle long-term performance has been ROEs around 19%-20%, and it has been very lumpy. I assume his future long-term performance will stay around 19%-20% and will keep on being lumpy. Gio

-

Yeah! Sure! If you are Mr. Buffett, Mr. Gates, Mr. Ellison, and very few others, certainly that might be the best policy… But how exactly it could be followed by anyone else, and still donate meaningful sum of money, I don’t understand… Anyway, I have never thought much about philanthropy, therefore I am most probably wrong. ;) Gio

-

--Mr. Brindle I'll keep buying. :) Gio

-

Yes I know. I wish I could find more public companies with the same characteristics of LRE, to diversify a little bit, but unfortunately I cannot… I plan to get an investment in LRE as large as the one I already have in FFH. That will be a full position for me, and I will stop there. Gio

-

Wonderful book! I keep it constantly on my desk. And reread at least 1 step each day! Can this be a good enough definition of 'bible'? ;) Gio

-

And if the stock downtrend keeps going on a bit longer, you might get a wonderful price too! :) Gio

-

;D ;D ;D Cheers! Gio Now that you are going to be getting many LRE dividends - you might go down to G.Lorenzi and buy me a nice present! Well, the answer to where do I keep finding all this money is I am a damn cheapskate! Sorry! ;D ;D ;D Gio

-

+1 Thank you very much for this idea! :) Gio

-

I will have reached a full position in LRE well before price gets to 1xBV. If and when price truly gets there, I won’t be buying no more, because Mr. Brindle will be buying in my stead like crazy! ;) Gio

-

;D ;D ;D Cheers! Gio

-

Thank you Williams406! Very useful! :) Gio

-

I have bought more at 6.65... but not that much!! ;D ;D ;D And I will keep buying. ;) Gio

-

Richard Brindle explains the power of three. http://www.lancashiregroup.com/investor-relations/lancashire-holdings-annual-results-2013.aspx Gio

-

March 2014 Report Gio 2014-March-Monthly-Report-TPRE.pdf

-

Maybe Dazel knows the name of the third party that might exercise ROFR until April 23, 2014. I admit I don’t know. Anyway… If I read the numbers correctly, the Genesee royalty would account for 22% of Altius’ 2015F royalty revenues, while the price Altius and its partners will have to pay, if the ROFR is exercised will be $251 million less than in the case it expires unused. Instead of $460 million, they will have to pay only $209 million. A 22% decrease in revenue vs. a 55% decrease in price… Not bad! ;) Furthermore, the cash Altius will have then at its disposal might be used to buy other royalties, not necessary tied to coal production, diversifying even further its royalties portfolio. Now that Altius has to buy 100% of CDP, it might not be a bad idea to use some cash for the purchase of royalties not tied to coal production. Are my numbers correct? Am I missing something? Gio

-

Do me a favour, never ever, ever, ever... say this again for a stock I own... :-) I will likely sell tomorrow after your post... Me, I don’t care much about the short and medium term… On the contrary, you know what? I really hope to lose money in the short and medium term! So that, as long as my view on ALS business model doesn’t change, I get to average down and to buy more shares cheaply: I am sure this way the money I will make in the long run will be greatly enhanced! And I don’t think I only talk the talk… instead, I think I walk the walk too! Just look at what I am doing with Lancashire… I sincerely hope I get the chance to replicate that same process of buying at lower and lower prices with Altius too. As long as I am right about Lancashire and Altius business models, I am getting very rich. ;) Gio

-

I also have bought more today... and, if the price keeps declining, I will buy more tomorrow... and more the day after tomorrow... but I am not a groupie!! ;D ;D ;D Yes! Of course we will meet at the Fairfax meeting! ;) Cheers, Gio

-

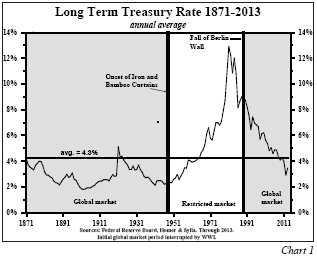

Sincerely, I have yet to find an attempt to justify present market valuations with some merit… If you look at the chart about Average Investor Equity Allocation, the author compares nowadays with the early 1980s, saying that situation couldn’t be repeated because interest rates were much higher back then. Yet, that same chart shows something very similar in the early 1950s… and during that time interest rates were as low as they are today (see the attached chart)… Then, the author goes on saying that, even if a 50% market crash were to come, it wouldn’t last years or decades… ??? ??? Who cares?!? What anyone should worry about is to have cash when good quality assets are marked down, exactly because the time frame at your disposal to take advantage of that situation will always be very limited!! Listen, say whatever you want, I agree with Mr. Klarman: We are swimming against the tide… So better choose among 2 strategies: 1) To be an incredibly smart stock picker, a la Packer; 2) To invest in something whose future results won’t depend at all on what the stock market does, a la Lancashire. Strategy n.2 is what Mr. Buffett is concentrating on since the late 1990s, preferring the purchase of whole operating businesses to the stock market, unless the stock market were hit hard (2003, 2009). Original mungerville, I am buying more Lancashire today too. ;) Gio

-

2014 FFH Shareholder's Dinner - Less Than 25 Tickets Left!

giofranchi replied to Parsad's topic in Fairfax Financial

Though it is a pity we won’t have the chance to meet in person this year, don’t worry Liberty! I plan to make the trip every year from now on! :) I spend so much time discussing ideas with all of you, and it is time I cherish so much, that, if possible, I truly want to meet you at least once a year! Therefore, Liberty, I sincerely hope next year will be the right time… Until then, keep up the good work! ;) Cheers, Gio