giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by giofranchi

-

It is pleasantly surprising to realize how much flirtatious Mr. Ben Franklin was with women! Always, of course, in a very gentlemanly manner! He simply enjoyed to talk to and to spend his time among women. One more trait I gladly share with this man born 270 years before I came into this world! ;D ;D ;D Gio

-

Hoisington Quarterly Review and Outlook First Quarter 2014 Gio HIM2014Q1NP.pdf

-

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

I think VRX market cap could be somewhat an issue, but much less of an issue than a lot of people think right now. Much more important imo is that Mr. Pearson still has a 30 years working life in front of him: many tools at his disposal to go on creating value for shareholders. Gio the interesting thing here is that VRX is still not very well known by most investors, and that includes most large investors. so the discovery process is still ahead of it. This combination will ignite their interest. Big investors need to build a trust relationship with a company before they invest. That's why I think the chance for multiple expansion is great. One the key things I've learned in watching markets for almost 30 years is that the big boys move Slow. We have a huge advantage. Yes! I agree. But also do not forget how Mr. Rockfeller truly became the wealthiest man in history: splitting up Standard Oil! Ok, Mr. Rockfeller might have been somehow forced to do so… And probably he would have never split his company up, if left alone… nonetheless, it worked just wonderfully! And he clearly understood it too! If you read his biography, you will find that, as soon as he heard the news that the injunction by the government to subdivide Standard Oil into many smaller companies had finally become reality, Mr. Rockfeller advised a friend of his, telling him: “Buy the stock!” ;) Contrary to what most people believe, I think each single business VRX has acquired (and will acquire in the future), after Mr. Pearson has applied to it a strict but rationale cost cutting discipline, might turn out to be much more valuable, as a single entity, than it was before VRX acquired it. In other words, when VRX finally gets too big, a tremendous amount of shareholders value could still be generated trough spin-offs. Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Maybe… Though going on I don’t see all those tools to keep creating value for shareholders at Inbev that I see instead at Valeant. Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

I think VRX market cap could be somewhat an issue, but much less of an issue than a lot of people think right now. Much more important imo is that Mr. Pearson still has a 30 years working life in front of him: many tools at his disposal to go on creating value for shareholders. Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Valeant Pharmaceuticals Announces Nominations For Board Of Directors http://ir.valeant.com/investor-relations/news-releases/news-release-details/2014/Valeant-Pharmaceuticals-Announces-Nominations-For-Board-Of-Directors/default.aspx Gio -

I think once again Mr. Einhorn put it best citing Gertrude Stein at the end of Greenlight Capital Q1 2014 letter: ;) Gio

-

I read one step each morning... over and over again. ;) Gio

-

Easy Eurozone Trades Are Running Out Of Road by Mr. Charles Gave Gio Daily+4.22.14.pdf

-

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Yes! This is exactly how I look at VRX's future sources of value creation too! wellmont imo is always right on the spot! ;) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Is $9.5 your estimate or was this number mentioned by VRX? the slides suggest $10.75 pro forma 2014 cash eps (can someone verify?) $9.5 was nothing but a (conservative) guess of mine… If the actual number is $10.75, yesterday I almost doubled my investment in VRX at a multiple of 12.5x. Extremely difficult to find such a high quality company trading at such a low multiple in today’s market! ;) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

I was just kidding, of course! ;) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Hey! Come on! You believe Mr. Ackman… and you don’t believe me?!?! ;D ;D ;D Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Great! Thank you! :) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Cristoforo, Do you know if Ackman’s presentation is downloadable in pdf format? Thank you, Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

I like the medical aesthetic business very much. If, following this acquisition, VRX revises Cash EPS upward to $9.5 (from $8.5, circa a 12% increase), we are still paying a multiple of 14x. Not bad, given all the prospects for future growth. Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

I have just bought more VRX. Gio -

I had in mind the slide in attachment. :) Half 2012 and the whole 2013 are not included. Gio

-

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Yeah! I am sort of a monotonous guy… all the companies I invest in look alike! ;) Cheers, Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Thanks Dazel, Though VRX is a relatively small position for me, much smaller than ALS. ;) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Thank you for posting this! And I agree… though, I guess he should get in shape a little bit… Come on, Mr. Pearson, after all you are only 54! ;) Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

Valeant Proposes to Combine With Allergan for $48.30 in Cash and 0.83 Shares of Valeant Stock for Each Allergan Share http://ir.valeant.com/investor-relations/news-releases/news-release-details/2014/Valeant-Proposes-to-Combine-With-Allergan-for-4830-in-Cash-and-083-Shares-of-Valeant-Stock-for-Each-Allergan-Share/default.aspx Gio -

VRX - Valeant Pharmaceuticals International Inc.

giofranchi replied to giofranchi's topic in Investment Ideas

lu_hawk, there is only one reason why an investment is a bad one: too high a price. But, today you are paying too high a price for VRX only if results from acquired businesses materially disappoint going forward. That’s why I said: show me the reasons those investments are bad ones! You say it is too early to judge? Well, how could you be bearish then? And, moreover, as investors we try to recognize the value and/or the pitfalls of any investment well in advance they have become obvious to everyone else! That’s what we do. Why, then, not to analyze each single acquisition VRX has made during the last 5 years, and try to judge if it has been wise to purchase that business, or vice versa it has been a foolish move? That’s what I am asking short sellers: analyze each acquisition and show me why most probably it will turn out to be a bad one in the future. Gio -

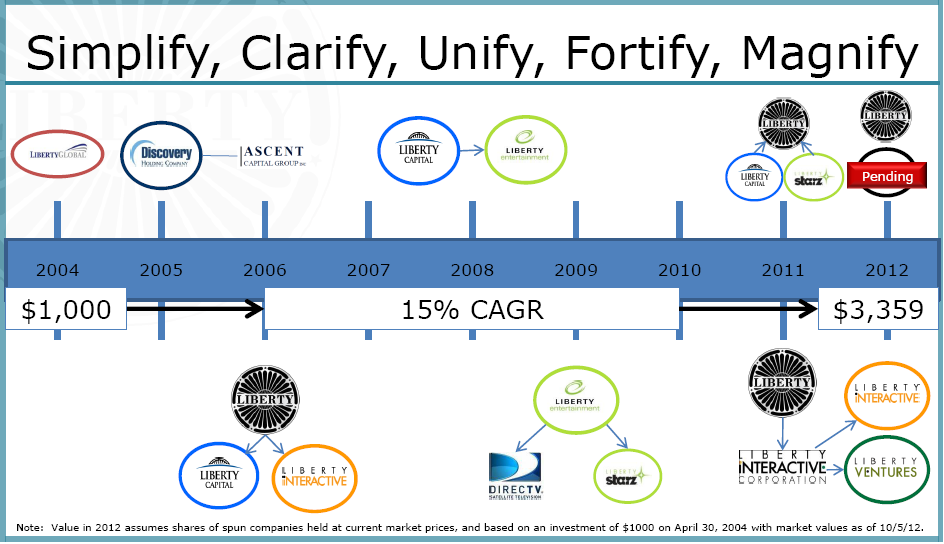

I think about LMCA this way: An hedge fund run by one of the shrewdest capital allocators out there, who is 10 years younger than Mr. Buffett (and therefore might still be at the top of his game for many years to come), and who has mastered probably better than anyone else the art of stock repurchases and the art of spin-offs engineering, both sources of value creation no hedge funds I know of can claim to possess nor benefit from. On top of that shareholders see a cost structure that is far less expensive than the 2% + 20% formula adopted by most hedge funds. Despite the fact LMCA has compounded capital at 15% since 2004, it is trading at a discount to its NAV. Of course, anything can happen, but it is very difficult to see how this could turn out to be a poor investment! ;) Gio

-

I am buying more LMCA as the market opens: right now it is the most undervalued company among the ones I am interested to invest in. :) Gio